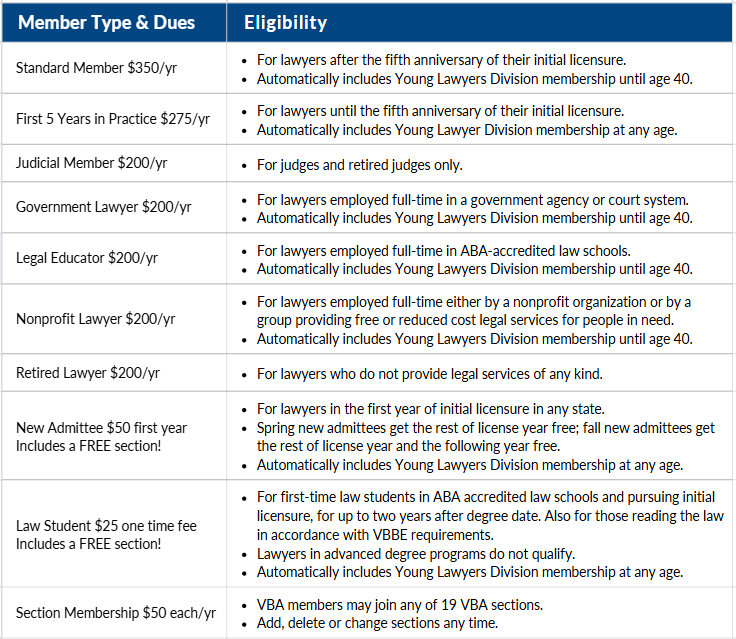

No matter your experience or your practice area, there’s a VBA membership for you!

Membership dues are not deductible as a charitable contribution but may be deductible as an ordinary and necessary business expense. The VBA estimates that 12% of basic dues support lobbying activities as defined by Section 13222 of the Revenue Reconciliation Act of 1993. Therefore, 88% of your dues may be deductible.

.png) Join the VBA

Join the VBA

.png) Your Support Matters

Your Support Matters

Learn More

Learn More